As we enter 2026, developing accurate cash flow projections is a critical step in guiding financial decisions and managing risk. These projections require careful consideration of accounts receivable, accounts payable, and prepaid expenses, as well as the assumptions that underlie them. At the same time, constructing strong 2025 year-end balance sheets provide the foundation for these projections by clearly capturing the operation’s financial position as books close for the year. Together, year-end balance sheet preparation and forward-looking cash flow planning help identify potential liquidity constraints, opportunities for improvement, and strategic actions that may be needed to position the business for a successful 2026.

Accounts Receivable

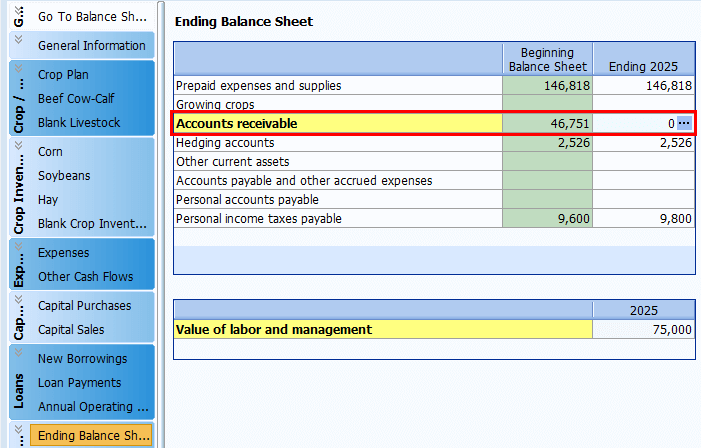

When working on the 2026 cash flow projection (FINFLO) it is important to keep in mind what has been documented on the 2025 year-end balance sheet. Any outstanding accounts receivable at year-end represent cash that is expected to be received in the upcoming period and should therefore be included as income in the cash flow projection. Therefore, 2025 year-end accounts receivable should be documented as income in the 2026 cash flow projection. To avoid double counting, consideration should also be given to whether any receivables have an impact on other revenue entries in the cash flow projection. This is often not the case, but something to keep in mind. Under the FINFLO section labeled ‘Ending Balance Sheet’, the 12/31/25 balance sheet value (labeled as ‘beginning balance sheet’) for accounts receivable should be reviewed (see screenshot below). Was the accounts receivable balance at a ‘normal’ operating level for the year? If no, an appropriate adjustment to the accounts receivable balance should be made, ensuring that the 2026 cash flow projection accurately represents the operation’s financial position. An example of an account receivable is the Farmer Bridge Assistance payment. The payment is to be recorded on the 2025 year-end balance sheet as an account receivable because it has been earned but will not be received until 2026. Accordingly, it will appear as a cash inflow in 2026 and should be reflected in cash flow projections for that year.

Accounts Payable

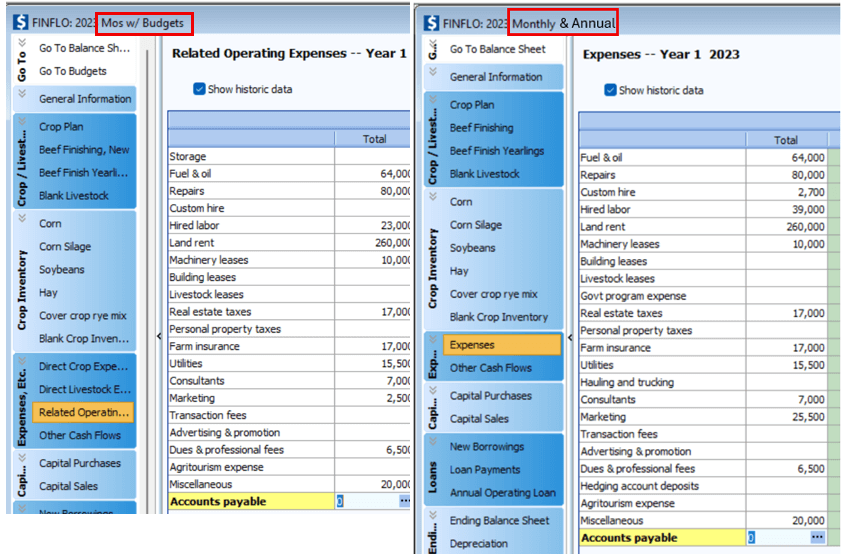

The accounts payable balance also plays an important role in cash flow projections (FINFLO). Outstanding payables at 2025 year-end represent expenses that will require cash payments during the 2026 projection period. The 2025 payables should be reflected as an expense in the 2026 cash flow projection. In FINFLO the related operating expense category labeled ‘Accounts Payable’ is the amount that is to be paid during the duration of the plan. When entering detailed data for the projected accounts payable under the expense section (called the ‘related operating expense’ section in FINFLO monthly with budgets) remember that the ‘Select from balance sheet detail’ option (a button that pulls values from the beginning balance sheet) is available. It is also important to consider whether these payable amounts are already captured in other projected expense items to avoid double counting. An example of double counting occurs when an outstanding veterinary bill is recorded on the balance sheet and included as a veterinary expense. When entering data into the FINFLO section ‘ending balance sheet’ the accounts payable balance on the 12/31/25 balance sheet should be evaluated to determine whether it reflects a ‘normal’ operating level for the farm. If the balance is not at a level typical for that farm, adjustments should be made to bring it back to the normal expected value. This ensures that 2026 cash flow projection (FINFLO) accurately represents the operation’s financial position.

Prepaid Expenses

When preparing cash flow projections (FINFLO), it is important to consider reducing the amount of prepaid expenses, particularly when the farm’s ending balance sheet shows prepaids that are higher than ‘normal’ for the operation or if the farm plans to reduce the amount of prepay activity based on their current financial situation.

For both annual and monthly projections, it is important to distinguish between what has already been paid in advance and what will require actual cash expenditure during the projection period.

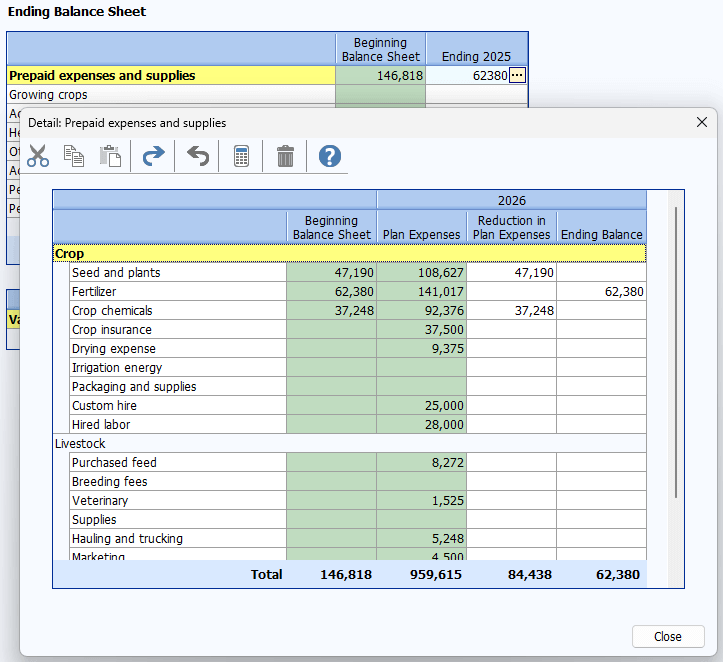

For example, if the farm carries a large amount of prepaid fertilizer on the ending balance sheet, the projection should reflect the cash that will actually be spent on fertilizer during the year, not the total value of fertilizer used. In addition, adjustments to the ending balance sheet section may be needed if the prepaid value as of 12/31/25 is larger than what is typically expected for the operation. Under the detail on the prepaid expense line for the ‘Ending Balance Sheet’ section there is a list of expenses and supplies that reflects the detail that was written for the 12/31/25 balance sheet (in some cases there is no detail), where individual adjustments can be made. In the case of high prepaids, the prepaid balance should be reduced to the correct value for the operation at year-end to better reflect ongoing operating conditions and avoid overstating future cash needs.

For a monthly cash flow projection with budgets, special care is needed when prepaid expenses from the prior year are higher than normal. Budgets typically reflect a ‘typical’ annual input expense, but if the farm carried excess prepaids into the year, it may plan to ‘use up’ some of those inputs rather than purchase as much new product with cash. In that case, the projected cash expense should be reduced accordingly. In the ‘Ending Balance Sheet’ data entry detail, the balance sheet value for each prepaid input can be compared with the cash expenses implied by the budget. The ‘Reduction in Planned Expenses’ column can then be used to adjust what cash will actually be spent during the projection plan (see screenshot below). At the same time, the ending balance sheet value for the prepaid item should be adjusted to the level expected at year end. It is also important to note that if detail is entered for any one of these prepaid inputs, it must be entered consistently for all the inputs.

Summary

Accurate cash flow projections (FINFLO) for 2026 depend on careful alignment between the 2025 year-end balance sheet and projected cash activity. Special attention should be given to accounts receivable, accounts payable, and prepaid expenses to ensure cash inflows and outflows are not overstated. By adjusting these items to reflect ‘normal’ operating levels and realistic cash activity, producers can develop more reliable cash flow projections.

Connect with FINPACK

Don’t forget to follow FINPACK on Facebook and Instagram, or connect with us on LinkedIn, and be sure to subscribe to FINPACK News email updates.

Coryn Davidson is an Extension Economist at the Center for Farm Financial Management in the Department of Applied Economics at the University of Minnesota. Coryn has a Bachelor’s Degree in Agricultural Business from the University of Wisconsin-River Falls and a Master’s Degree in Agricultural Economics from Colorado State University. She has experience in extension work through her 2023 AmeriCorps service and has also been part of a farmer educational program through ‘Farmer Campus’. Coryn’s interests include farm financial management, enterprise analysis, and economic impact assessment. She has an agricultural background in both dairy and mixed produce production.